Page 14 - afs12

P. 14

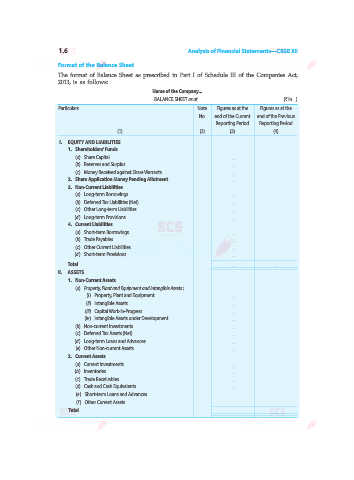

1.6 Analysis of Financial Statements—CBSE XII

Format of the Balance Sheet

The format of Balance Sheet as prescribed in Part I of Schedule III of the Companies Act,

2013, is as follows:

Name of the Company...

BALANCE SHEET as at... (` in ...)

Particulars Note Figures as at the Figures as at the

No. end of the Current end of the Previous

Reporting Period Reporting Period

(1) (2) (3) (4)

I. EQUITY AND LIABILITIES

1. Shareholders’ Funds

(a) Share Capital ... ...

(b) Reserves and Surplus ... ...

(c) Money Received against Share Warrants ... ...

2. Share Application Money Pending Allotment ... ...

3. Non-Current Liabilities

(a) Long-term Borrowings ... ...

(b) Deferred Tax Liabilities (Net) ... ...

(c) Other Long-term Liabilities ... ...

(d) Long-term Provisions ... ...

4. Current Liabilities

(a) Short-term Borrowings ... ...

(b) Trade Payables ... ...

(c) Other Current Liabilities ... ...

(d) Short-term Provisions ... ...

Total ... ...

II. ASSETS

1. Non-Current Assets

(a) Property, Plant and Equipment and Intangible Assets :

(i) Property, Plant and Equipment ... ...

(ii) Intangible Assets ... ...

(iii) Capital Work-in-Progress ... ...

(iv) Intangible Assets under Development ... ...

(b) Non-current Investments ... ...

(c) Deferred Tax Assets (Net) ... ...

(d) Long-term Loans and Advances ... ...

(e) Other Non-current Assets ... ...

2. Current Assets

(a) Current Investments ... ...

(b) Inventories ... ...

(c) Trade Receivables ... ...

(d) Cash and Cash Equivalents ... ...

(e) Short-term Loans and Advances ... ...

(f ) Other Current Assets ... ...

Total ... ...